The last few months have brought us a few meaningful AI developments that will materially change how we interact with software, which in turn affects where value accrues within the software ecosystem. Allow me to explain.

Some context…

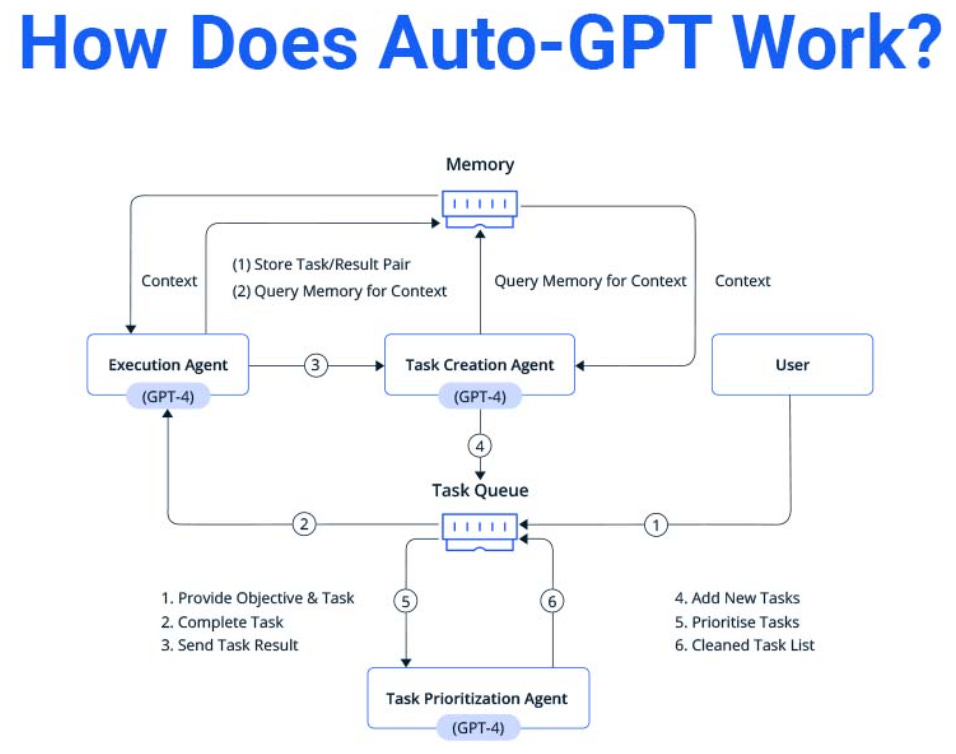

Ever since the ChatGPT moment for LLMs, people have understood the possibility of autonomous software bots that could complete tasks on behalf of users. Projects like AutoGPT were spun up to begin to explore how these autonomous programs would work.

Natural language prompts would replace traditional SaaS GUIs as the medium for instructing software on a desired outcome. Early examples were content creation, basic market research, and personal shopping. “Go find me some Nike Dunks between $100 and $150”. AutoGPT would break down the overarching task into subtasks (create evaluation criteria, search through relevant sites, document prices, return links back) and leverage an Execution Agent to complete the task.

While there were some impressive early results, it struggled to be useful for anything in a way that made it worth leveraging in production. There were issues around memory (shorter context-windows back then) and suboptimal task decomposition (no reasoning models yet), but most of where people had issues was tool use. Execution Agents within the AutoGPT framework would clumsily call APIs, access file systems, browse websites (via HTML surfing), and incorrectly parse Google results. Most of these problems stemmed from the fact that the core Execution Agent didn’t have any repeatable way of accessing the core services associated with tasks it was being assigned by the Task Prioritization Agent.

What ultimately arose from the AutoGPT effort was an understanding that agent-based systems needed to have some additional understanding of how to leverage tools outside of whatever pre-training came within the model. So since then, we have seen concerted efforts by companies to build pre-configured agents that are tailored to handle a specific task. This works! But it won’t scale us to the truly autonomous future that so many had envisioned since the early days of AutoGPT. Why? If each tool a platform wants to be able to call has to have its own bespoke agent, then companies will constantly have to build and maintain a library of custom agents. As Addy Osmani put it eloquently in a recent piece, “…the bottleneck was no longer the model’s intelligence, but its connectivity”.

So what’s changed?

MCP has changed how we will interact with third-party tools. An open protocol allows everyone to standardize the way in which their core services are accessed. There are real similarities to what OpenAPI did for API design and specs. They both standardized the way in which we interacted with core services - solving the idiosyncrasy issue that had plagued APIs and agent / tool communication.

A lot has been said about what MCP means for the future of agents, so I will try and be succinct here. In short, if we assume that accessing tools becomes a solved problem, then agent-based platforms can focus on more of the core architectural issues that had plagued these systems in the past - memory, reasoning etc. Importantly, platforms can also now focus on the tools that deliver the best outcomes, not just the tools that are the easiest to access. Which brings me to my next point…

Agent <> tool connectivity will shift the balance of power toward conduit companies

What do I mean by conduit company? A conduit company is a company whose inherent benefit is the access and orchestration of tools to complete an outcome. They are the conduits for each new successive advancement in foundational models and tool capabilities. Notably, these companies own the customer. By owning the customer, they will become the core way that many customers will access tools.

Take an AI scheduling assistant that can book reservations for you via Resy and block out the appropriate time via Google Calendar. Previously, customers would have had to access each of these apps individually and interact with them via whatever SaaS GUI was provided. Now, the AI assistant has taken over that relationship with the apps themselves.

The conduit companies will eventually disassociate the relationship between customer and tool. This has serious ramifications:

Tools whose core differentiator is UI / UX may struggle in a world in which they are solely being accessed via conduit companies

Transactional tools, i.e. tools in which customer relationships are brief and monetary, will face serious price pressure as they can be subbed out by the conduit company

To that point, data and usage moats become increasingly valuable as ways to continue to be leveraged by end customers even if direct relationships are severed

Tools may now prioritize relationships with the conduit companies instead of the end customer

While some people, like Gokul Rajaram, rightly point out that MCP is a double-edged sword that may cause companies to think twice about implementation, I think classic prisoners’ dilemma will force everyone’s hand. Yes, if every tool company decides to forgo MCP, then the conduit companies will lack the same sort of leverage if their access is throttled. But if just one company in a market decides to prioritize agent connectivity and become the preferred vendor for a conduit company, then it may force other companies within a market to cave.

As always, if you are building a startup that fits my conduit description, or anything else leveraging tool-augmented agents, please reach out at nickb at northzone dot com.